Download 51A125 Kentucky Template

Download 51A125 Kentucky Template

Filling out the 51A125 Kentucky form is a straightforward process, but it requires careful attention to detail. This form is specifically for organizations that qualify for a sales and use tax exemption. After submitting the form, the Department of Revenue will review your application. If approved, you will receive a letter of authorization with further instructions.

When filling out the 51A125 Kentucky form, it's essential to follow specific guidelines to ensure your application is processed smoothly. Here’s a list of things you should and shouldn’t do:

| Fact Name | Description |

|---|---|

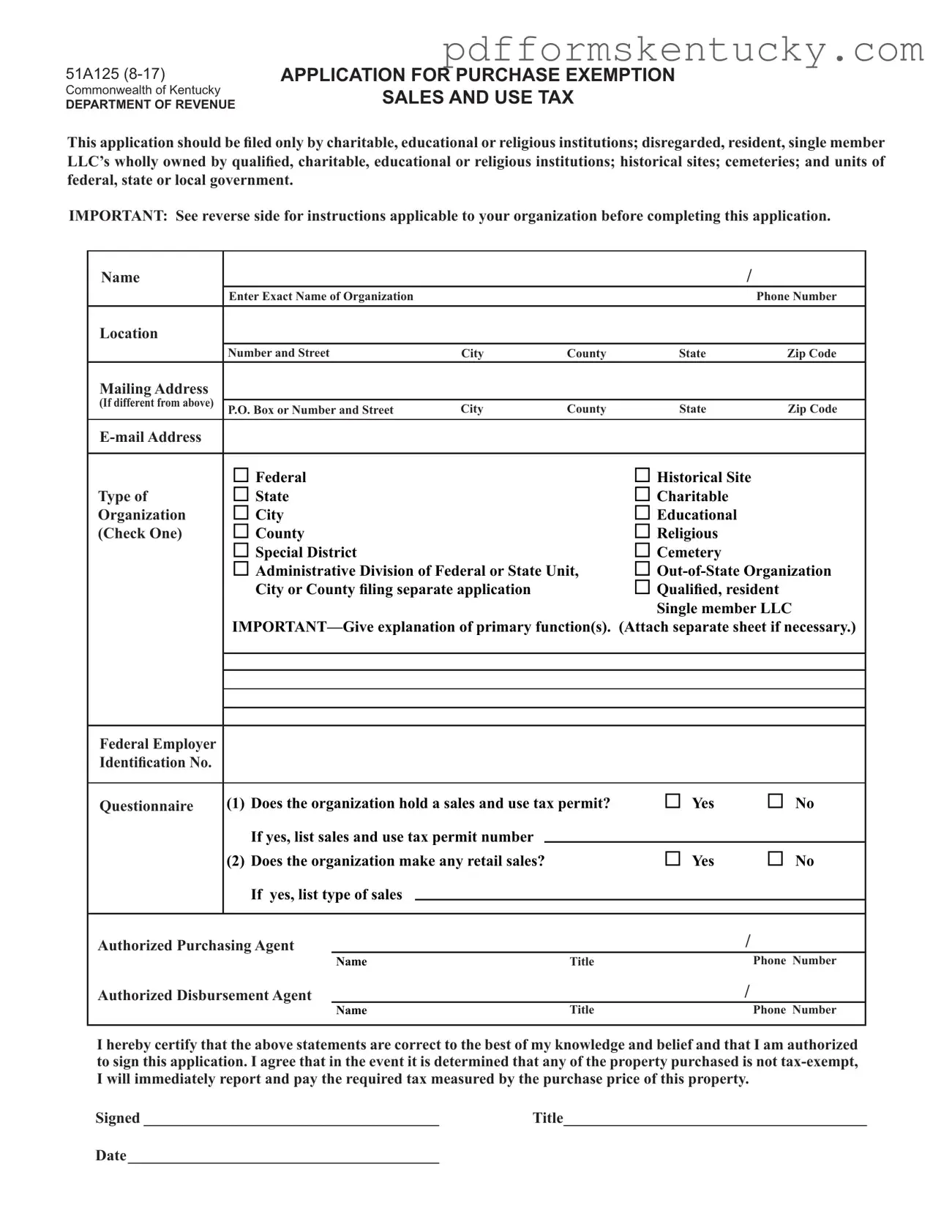

| Form Title | Application for Purchase Exemption Sales and Use Tax |

| Governing Laws | KRS 65.005 and Section 501(C)(3) of the Internal Revenue Code |

| Eligible Applicants | Charitable, educational, or religious institutions; historical sites; cemeteries; and government units. |

| Application Requirement | Must include Articles of Incorporation and a detailed schedule of receipts and disbursements. |

| Sales Tax Permit | Organizations must indicate if they hold a sales and use tax permit. |

| Tax Exemption Scope | Exemption applies to purchases for exempt functions; other purchases may be taxable. |

| Notification Requirement | Any changes in name, address, or nature of the organization must be reported to the Department of Revenue. |

| Submission Address | Kentucky Department of Revenue, Division of Sales and Use Tax, P.O. Box 181, Station 67, Frankfort, KY 40602-0181 |

| Out-of-State Organizations | Must provide proof of exemption from sales tax in their home state. |

The 51A125 form is essential for organizations seeking a sales and use tax exemption in Kentucky. However, several other documents often accompany this application to ensure compliance and provide necessary information. Below is a list of these forms and documents, each serving a specific purpose in the exemption process.

Each of these documents plays a critical role in the application process for tax exemption in Kentucky. Ensuring that all required paperwork is submitted can help streamline the approval process and avoid potential delays.

Kentucky Amended Tax Return - The form specifies different calculations for filing jointly or separately.

To facilitate the employment verification process, you can access resources that provide templates and guidance; for instance, the smarttemplates.net/fillable-california-employment-verification/ offers a fillable version of the California Employment Verification form, which can simplify compliance for employers.

Wraps Ky - Filing with the original form ensures that the Department of Workers Claims recognizes the withdrawal.

Kentucky State Taxes - Retaining a copy of the submitted form is advisable for personal records.

What is the 51A125 Kentucky form used for?

The 51A125 form is an application for purchase exemption from sales and use tax in Kentucky. It is specifically designed for charitable, educational, or religious institutions, as well as certain government entities and historical sites. By completing this form, eligible organizations can apply to make tax-exempt purchases related to their exempt functions.

Who is eligible to file the 51A125 form?

Eligibility for filing the 51A125 form includes charitable organizations, educational institutions, religious entities, historical sites, cemeteries, and units of federal, state, or local government. Additionally, disregarded, resident, single-member LLCs wholly owned by qualified organizations can also apply. It's essential that the organization meets the criteria outlined in the form to qualify for the exemption.

What documents must accompany the 51A125 application?

Depending on the type of organization, specific documents are required. Charitable, educational, and religious institutions must attach a copy of their Articles of Incorporation, a detailed schedule of receipts and disbursements, and a letter from the IRS confirming their tax-exempt status under Section 501(C)(3). Historical sites need to include a letter from the Kentucky Heritage Commission confirming their listing in the National Register. Cemeteries must provide similar documentation, including a property tax exemption ruling.

How does an organization know if its application is approved?

If the application is approved, the organization will receive a letter of authorization that includes an exemption number. This letter will also contain instructions for claiming the exemption on future purchases. It’s important to keep this letter on file for reference when making tax-exempt purchases.

What happens if the organization makes taxable sales?

If the organization engages in taxable sales and is not classified as an educational or charitable institution, it will need to obtain a sales and use tax permit. This is crucial to ensure compliance with Kentucky tax laws and avoid potential penalties.

Can out-of-state organizations apply for the exemption?

Yes, out-of-state organizations can apply for the exemption using the 51A125 form. However, they must also submit a copy of their exemption letter or authorization from their home state to prove their tax-exempt status. This additional documentation is necessary for the Kentucky Department of Revenue to process their application.

What should an organization do if there are changes in its information?

It is vital for organizations to promptly notify the Kentucky Department of Revenue of any changes in their name, address, or the nature of their organization. Keeping this information current ensures that the organization remains compliant and can continue to benefit from its tax-exempt status.

Where should the completed 51A125 form be mailed?

The completed 51A125 application should be mailed to the Kentucky Department of Revenue, Division of Sales and Use Tax, at P.O. Box 181, Station 67, Frankfort, Kentucky, 40602–0181. Ensuring that the application is sent to the correct address will help avoid delays in processing.